Oil to $120 Again?

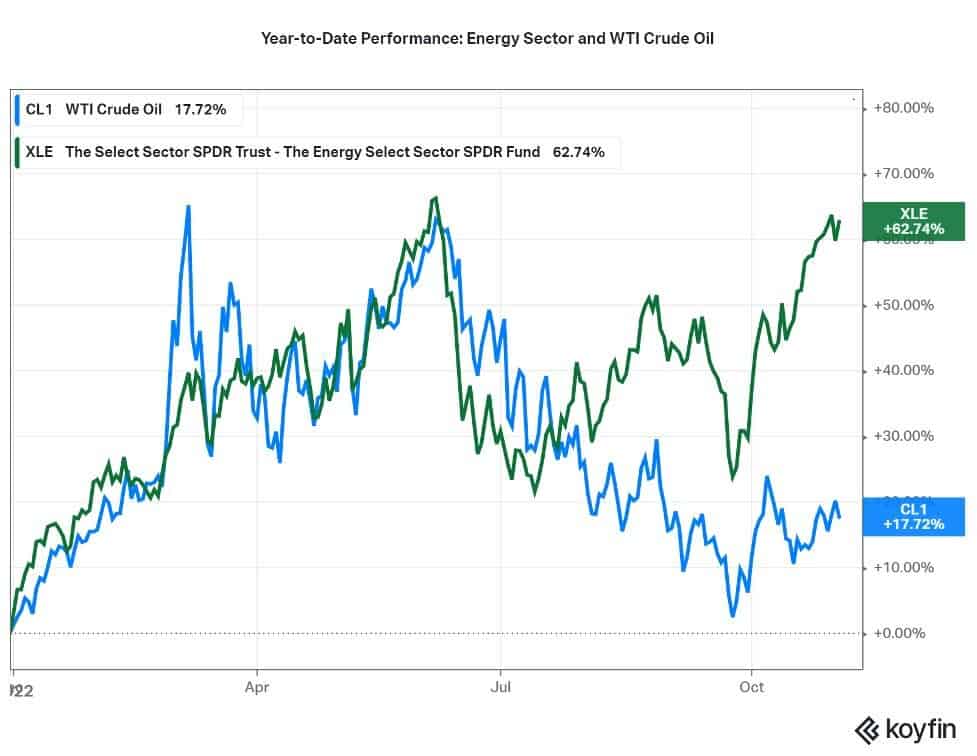

Energy remains the only green sector for 2022, and while it has risen 68% since January 1st, it remains our preferred sector in the market. Much of the equity movement for the first half of the year followed closely with oil prices, but now that we have witnessed promising earnings reports for three quarters of 2022, energy stocks have risen above and beyond oil prices. We believe the sector will continue to benefit from rising crude prices and we anticipate oil, both Brent and WTI, to advance going into year-end and the beginning of 2023. It is very possible we will see $120 WTI again (that target was hit on March 7th and June 7th of this year). Several factors contribute to this thesis, as we’ll outline below, and while this isn’t a positive signal for your gas bill, we think the returns to our equities should more than cover that extra cost at the pump.

A gloomy macroeconomic outlook provides some headwinds to the sector, but the end of the SPR release, degradation of Russia’s oil infrastructure, a (likely) falling dollar, OPEC+ production cuts, and the potential re-opening of the Chinese economy support our outlook for higher oil prices. The biggest economies in the world are headed into the winter months, and oil and natural gas seem very likely to rise, substantially.

Past performance is not a guarantee of future results. The information provided should not be considered a recommendation to purchase or sell any particular security.

The Strategic Petroleum Reserve: A Cure for the Symptoms, Not the Problem

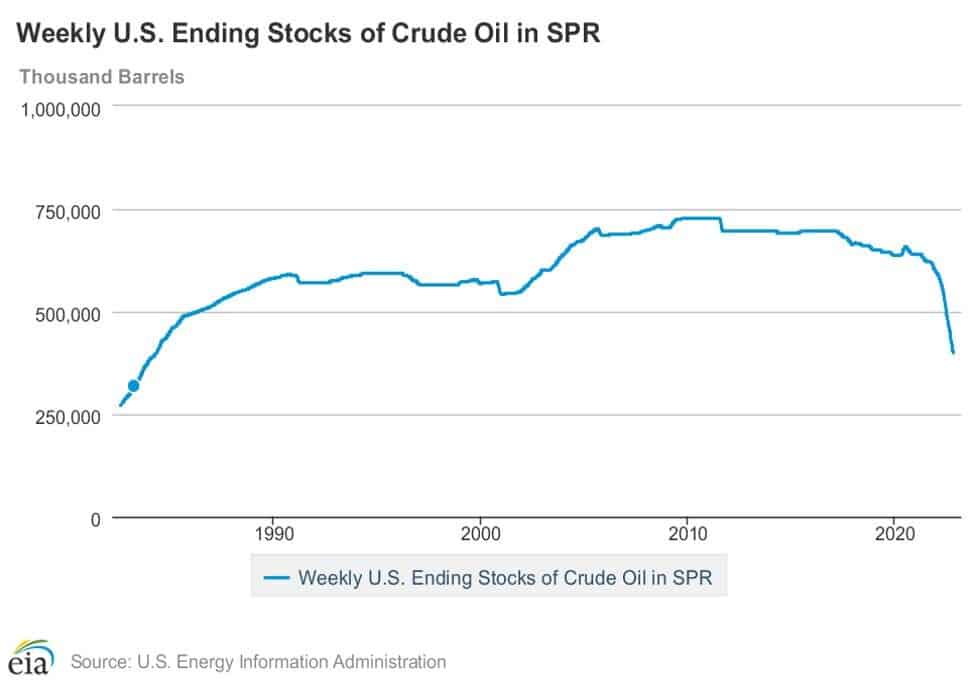

Perhaps the greatest boost to U.S. energy prices will come through the end of releases from our Strategic Petroleum Reserve (SPR). In an effort to reduce gas prices at the pump, the Biden administration has been depleting the U.S. SPR by 1 million barrels per day since March of this year. This marked the largest release of oil from the strategic reserves in U.S. history. Following a final 15 million barrel auction to major U.S. oil companies, the effort has concluded with a total of 180 million barrels that have been released to the market. To put this volume into perspective, the United States typically consumes almost 20 million barrels per day. A 5% boost to our typical oil supply has created downward pressure on energy prices but has also left the SPR at its lowest point in almost 40 years.

At some point, the U.S. will have to refill the reserve. The SPR is critical in the case of unforeseen natural disasters, wartime demand requirements, or other unnatural disruptions to energy supply or demand. President Biden says that the SPR will be refilled once oil prices drop at or below $67 to $72 per barrel, but this may have to be done much sooner. Regardless of when we choose to refill what’s been depleted, without the SPR release subsidizing supply, the 1 million barrel per day void will most certainly lead to higher crude prices. In addition to the U.S.’ reserve depletion, allied nations have released 60 million barrels of their own reserves for the same purpose. While there’s no guarantee that we’ve seen the last of reserve releases, there are no planned releases for the coming months and supply should tighten on the global stage.

Russian Oil Embargos and Price Caps

Prior to the Russia-Ukraine war, Russia was the world’s third-largest oil producer and second-largest exporter, reaching a 2020 annual average of 10.5 million barrels produced per day. While Russian petroleum is still finding end markets, the lack of availability of replacement parts and maintenance of Russia’s fields is causing a consistent decrease in the Russian supply. It is likely they have already lost previous production capacity and are probably closer to a 9.5 to 10 million barrel per day output now. The longer the Ukraine war is waged, the more likely it is that their production will continue to decline.

G7 countries have additionally agreed to set a price cap on Russian oil to limit Russia’s earnings while their assault on Ukraine continues. It is yet to be seen how much this will impact oil supply and prices but is yet another bullish indicator for the commodity.

Chinese Reopening

A final boon for energy markets is the anticipated reopening of the Chinese economy. In recent days, there have been murmurs of an adjusted Covid-19 policy and removal of the restrictive “zero-tolerance” stance China has taken since the onset of the pandemic. China is the second largest oil-consuming country next to the United States, so if its economy begins to run again, even if still below its potential, oil demand should sharply increase.

There is still a high likelihood that the government will continue to shift its Covid policy stance dynamically, but anything more lenient than the status quo would be positive for oil markets. The Chinese economy cannot remain locked down forever and the prospects of future investment in the country depend on a more rational Covid policy.

Conclusion

Just like all other assets this year, energy has seen volatility and should continue to do so. However, given what we’re seeing geopolitically on the supply and demand sides, we are happy to reiterate our confidence in the sector and our investments within it. Time will tell if we see oil above $120 again, but it will almost certainly remain in a range where our portfolio companies have the opportunity to see large margins and healthy profits. We will monitor the sector over the coming months, perhaps years, and as the macro picture for oil shifts, we will move strategically.

This material represents an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Past performance does not guarantee future results.

The value of commodity-linked investments may be affected by financial factors, political developments and natural disasters. As such, investment options that invest primarily in commodities may experience greater volatility than investments in traditional securities.