Overview:

Overview:

With recent volatility, I think a note on basic investing is valuable. First, markets move both up & down. Don’t get too elated when they make big moves up or too anxious when they make a big move down. Ask yourself if anything has really changed or is this a short-term reaction of traders. The difference between traders and investors is, over time, investors make money and traders do not. This does not mean that we will not reduce the size of positions and gather cash for future bargains, but wholesaling out of the market is almost always fruitless. The usual result is you catch a lot of the downside, or all, since no one can forecast the top or bottom, but usually you miss more of the upside than you missed of the down, resulting in a lot of activity which almost always results in lower returns and higher taxation.

I’ve examined years of client returns and this is almost always the case. It is human nature to want to be fully invested when things seem to be going strong and to be fully in cash when the market has a few bad days. The more one acts on those emotions, almost certainly, the lower the returns will be.

Ask yourself what has materially changed. If sectors are rotating due to macroeconomics, then I believe we should change with them. Remember, CNBC is there to keep you tuned-in. Almost every money manager who appears, is selling their book (wants you to buy what they own or sell what they are shorting). The hosts try to build a story around what is happening – but they are seldom accurate in their assessment and almost never get tomorrow correct.

Special Note: For MLP K-1s and the income tax forms associated with them, you may click on this link and download your specific forms. They should save you or your accountant time in preparing your tax return. Go to Tax Package Support for more information.

Our Strategy:

In the summer of 2008, we increased cash and equivalents to about 50% because there was a material reason to do so. Thousands of sub-prime, adjustable-rate mortgages were about to start resetting in September thru December. These were the type that paid nothing down and nothing at closing, had monthly payments at a 1% rate with 6% added to the mortgage each of the first two years. Add closing costs which were rolled into the mortgage and these mortgages were typically 20% plus higher than the inflated purchase price – there was simply no reasonable expectation that these would not result in foreclosure.

Today, we are watching our oil supply. Unfortunately, we are reliant on countries with large populations of radical Muslims to provide us with the oil to keep our country running. Vast oil and natural gas reserves are literally beneath our feet, nuclear power is available but has been shunned, while we send our money overseas, much of which goes to finance the terrorists that we spend hundreds of billions to fight. I hope that changes soon, but for now the question is how to protect and grow our investments in this environment.

We are gathering cash from investments that do not lend themselves to high-priced oil, to reduce our overall exposure and to provide us the opportunity to buy good companies cheap. It is an important distinction that we are not buying hot stocks, we are buying solid companies which are well-positioned to grow in a world where millions of people are moving from being peasants to middle-class citizens every month.

Mid-East & Oil Turmoil…

Egypt, Libya, Tunesia and other Middle East nations have a host of human and political issues, but the impact on our markets has been somewhat muted. They’ve had the effect of making a market rally pause while the price of oil has risen some $20/barrel. Though the reduction in Libyan crude is not of the magnitude to cause an oil shortage, it does increase the susceptibility of the crude oil markets to other potential supply shocks. If the political unrest were to spread to Algeria, we might see a further spike in oil prices as the combination of Libya and Algeria supply constraints would be larger than Saudi Arabia could cover. It is in the world’s and Libya’s interest to help General Gaddafi find a new (not so pleasant) home as quickly as possible.

Egypt, Libya, Tunesia and other Middle East nations have a host of human and political issues, but the impact on our markets has been somewhat muted. They’ve had the effect of making a market rally pause while the price of oil has risen some $20/barrel. Though the reduction in Libyan crude is not of the magnitude to cause an oil shortage, it does increase the susceptibility of the crude oil markets to other potential supply shocks. If the political unrest were to spread to Algeria, we might see a further spike in oil prices as the combination of Libya and Algeria supply constraints would be larger than Saudi Arabia could cover. It is in the world’s and Libya’s interest to help General Gaddafi find a new (not so pleasant) home as quickly as possible.

Shy of further contagion, we are likely seeing the near-term peak on oil prices, for Saudi Arabia has a vested interest in keeping the prices from rising so much that they choke the global recovery, or even worse, inspire the United States into adopting an energy policy which might reduce and eliminate our dependence on OPEC oil. Continued high oil prices should be bullish for natural gas since it is a low-cost, relatively clean energy source that is economically sensible. And now that Great Britain, the Eurozone, and the United States are all broke, I don’t believe we will see much movement towards solar or wind which require large government contributions to make them economic.

We have increased our holdings in the companies that do the drilling and service work on new wells as I suspect that big oil companies will have very active drilling programs with oil above $75 (right now most oil is priced around $115/bbl). You might call this the pick and shovel approach for it was the suppliers of basic tools who made the big and consistent money during the gold rush.

Still another area to watch is the copper market and infrastructure. Once the middle east settles, copper and other infrastructure related commodities and companies should rise quickly. This should give new money a chance to get in to some great companies that seemed to just keep running up, without giving new investors the opportunity to buy-in on a dip.

The dollar…

The dollar has long enjoyed its position as the world reserve currency. It has afforded us many luxuries such as cheap oil and gas and the ability to live beyond our means. Only now, our government has taken this to a level that the world will not tolerate. In 2005, our federal budget was $2.4 trillion. In 2010 it was $3.6 T and 2011 it is $3.8 trillion. $200 to $400 billion dollar deficits were uncomfortable, but last year and this year our federal government has seen fit to expand those deficits to $1.6 trillion each year! This does not count the Fed’s quantitative easing since their near $3 trillion is technically buying assets (of course most of those assets are IOU’s from the federal government. Don’t try this at home.

This seems to escape many if not most, Americans. Unfortunately, the traditional buyers of our debt fully understand that in the past two years the dollar has been printed and guaranteed future printing to the extent that it has fallen 20% against the Canadian dollar and the Swiss franc, over 30% against the Aussie and almost in half against gold. Even China is once again allowing their yuan to appreciate against the dollar. Just three years ago when the financial crisis began, the dollar was still viewed as a flight to safety. In fact for over 60 years, any time there was economic turmoil in the world, people would run to the dollar. Last year, when Greece was exposed, the flight to safety went to gold and the Swiss franc. Currently, with the middle east in turmoil, again the flight to safety went to gold and the Swiss franc. It is painfully obvious that the rest of the world is losing faith in our ability to pay our debts and fifty years from now it is very likely that this decade will be remembered as the decade that the dollar lost its status as the world’s reserve currency.

I know that sounds doom and gloom, but unfortunately that is exactly what is taking place. In fact, as much as Tim Geithner would like to convince you of our “Strong Dollar Policy”, he himself has chided China for keeping their currency undervalued. Congress and the President have done the same. Even Ben Bernanke said just two weeks ago that he was not responsible for inflation in emerging markets. He said “if they don’t want inflation, they should just let their currencies appreciate”. If we want everyone else to allow their currencies to appreciate against the dollar, we are practicing a weak dollar policy and the dollar will drop in value.

The silver lining (yes that is a hint) is that we do not have to be among the victims. Victims will include anyone holding cash savings, CD’s, bond mutual funds and long-term debt. If you are earning 3% in a CD, sending 1% to the IRS, leaving you with 2% earnings, while the dollar is declining in value by >10% per year, you have found a safe way to go broke without noticing. Using that scenario, you will lose 1/3 of your purchasing power in just five years. In ten years you could buy less than half as much. This is why we have so heavily weighted our portfolios towards companies that are not only profitable, but have hard assets. Hard assets will compensate you for the dollar’s devaluation. This is a sector rotation to hard assets and away from intellectual property and forms of cash.

In an environment where your currency is devalued, labor and intellectual property such as software and services, become cheaper while commodities and equipment become more expensive. I would rather own the things going up in value (probably does not need saying). By the same token, a bank holding a 30-year mortgage will actually make no money or even lose money on the mortgage. I believe as this unfolds, you will also find home prices stabilize and rise as astute investors realize that buying a house at or near construction cost and using a 30-year mortgage will almost certainly result in paying the mortgage with relatively worthless dollars in the future.

Again I may depress. But again, there is a silver lining. While the dollar burns, we do not have to be victims of the fiddling in Washington. There are many opportunities to insure our financial futures – they just require action. I believe our portfolios are well positioned to do just that. In fact, since rotating to this portfolio in early 2009 due to the new government spending and market conditions, we have considerably outpaced all major indexes. Of course there will be short periods when banks or computer makers or software does especially well and we will miss that, but I do not expect those times to be long in duration. The macro-picture of the world and of world currencies just does not support those sectors. They had their moments in the past two years, but had you owned the S&P 500 less those sectors, you would have out-performed the entirety of the S&P.

Again I may depress. But again, there is a silver lining. While the dollar burns, we do not have to be victims of the fiddling in Washington. There are many opportunities to insure our financial futures – they just require action. I believe our portfolios are well positioned to do just that. In fact, since rotating to this portfolio in early 2009 due to the new government spending and market conditions, we have considerably outpaced all major indexes. Of course there will be short periods when banks or computer makers or software does especially well and we will miss that, but I do not expect those times to be long in duration. The macro-picture of the world and of world currencies just does not support those sectors. They had their moments in the past two years, but had you owned the S&P 500 less those sectors, you would have out-performed the entirety of the S&P.

China…

Finally, the moment I’ve been waiting for… China has clearly begun to allow their currency to appreciate, again.

As QE2 started to cause inflation in China, they did what they always do to fight inflation. They raised their interest rates and raised bank reserve requirements. This is from the classic playbook for Central Bankers. It attacks inflation by choking down the economy. It has always seemed to me that a better alternative would be to allow your currency to appreciate with the economy. It fights inflation since each dollar or yuan is worth more so less are required to purchase a good or service. In effect, it makes your citizens richer – if your currency appreciates 20%, a $1,000 has the purchasing power of $1200, so income and savings become worth more and your citizens can purchase more goods, purchase gasoline cheaper, and boost the economy from within.

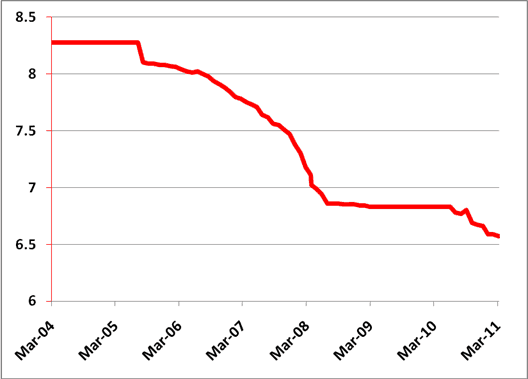

As you can see in this chart, China held the yuan firmly pegged around 8.35 yuan per dollar until July 2005. For the next three years they allowed it to appreciate an average of 7% per year. That continued until May of 2008 when the financial crisis erupted and China pegged the yuan again, but this time at 6.84 per dollar, almost a 20% appreciation in less than three years. The peg remained until a few months ago when the yuan began to appreciate just slightly, but now can be seen beginning to appreciate again at about an 8% annual rate.

As this continues, we will want to own companies who sell to these (richer) Chinese consumers. Whether the companies are domiciled in the United States, China, or some other country is of much lesser importance.

Hope you enjoy the longer and warmer evenings,

Frank

Disclosure: Nothing contained herein is to be considered a solicitation, research material, an investment recommendation or advice of any kind. The information contained herein may contain information that is subject to change without notice. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. Product suitability must be independently determined for each individual investor. Frank Beck & Beck Capital Management explicitly disclaims any responsibility for product suitability or suitability determinations related to individual investors. The investment products discussed herein are considered complex investment products. Such products contain unique risks, terms, conditions and fees specific to each offering. Depending upon the particular product, risks include, but are not limited to, issuer credit risk, liquidity risk, market risk, the performance of an underlying derivative financial instrument, formula or strategy. Return of principal is not guaranteed above FDIC insurance limits and is subject to the creditworthiness of the issuer. You should not purchase an investment product or make an investment recommendation to a customer until you have read the specific offering documentation and understand the specific investment terms and risks of such investment.

This material represents an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Past performance does not guarantee future results.