It’s hard to believe it’s already a new year. As always, each new year brings with it, new goals, new resolutions, and a new fresh outlook.

When considering this new year, I am reminded of the Grateful Dead lyrics, “What a long, strange trip it’s been,” since the start of 2022 is starting to look a lot like 2021 with a new COVID variant and a rock-n-roll start in the markets. I expect two things of 2022. First, the Omicron variant will substantially lead us to herd immunity. It is a milder COVID, relatively speaking, but it is highly contagious. That may actually be a blessing. Natural immunity amongst the masses (herd immunity) is what has ended every pandemic in our history. With that, and at least, a continual reopening of the world economies and gradual, but steady, improvement in the supply chain, I expect our portfolios to do well, regardless of Federal Reserve actions and D.C. So, like the Grateful Dead sang, let’s “Just keep truckin’ on” and welcome the promise that accompanies a new year.

Last year, we were bullish, and that paid off. We had a good year, while the 10-year Treasury bond had a negative total return. Like last year, we were bullish due to two themes. Our capitalized profit model indicated about 20% gain for the S&P 500 and our assumption that COVID restrictions would relax to an unknown extent by the end of the year. Today, our profits model indicates the S&P at 5275 and the Dow at 40,000 by year-end. We are expecting that to be bolstered by an economic end to COVID and a corresponding increase in corporate profits. Regardless, whether Omicron provides us herd immunity, or we just come to accept COVID like the flu, two yearsis more than enough. Life must go back to normal – people need to go back to work – and the supply chain will correct, decreasing the rate of inflation.In this issue, we will discuss:

- Contrary to media discussions, the Nasdaq often rises while interest rates rise

- Federal Reserve hikes, taper and the probable reduction in their balance sheet

- The supply chain and what some major corporations have already enacted

- Productivity gains and corporate net profits

- Inflation and how we are addressing it in our portfolios

- New uses of our Defined Parameter investments

Nasdaq & Rising Interest Rates

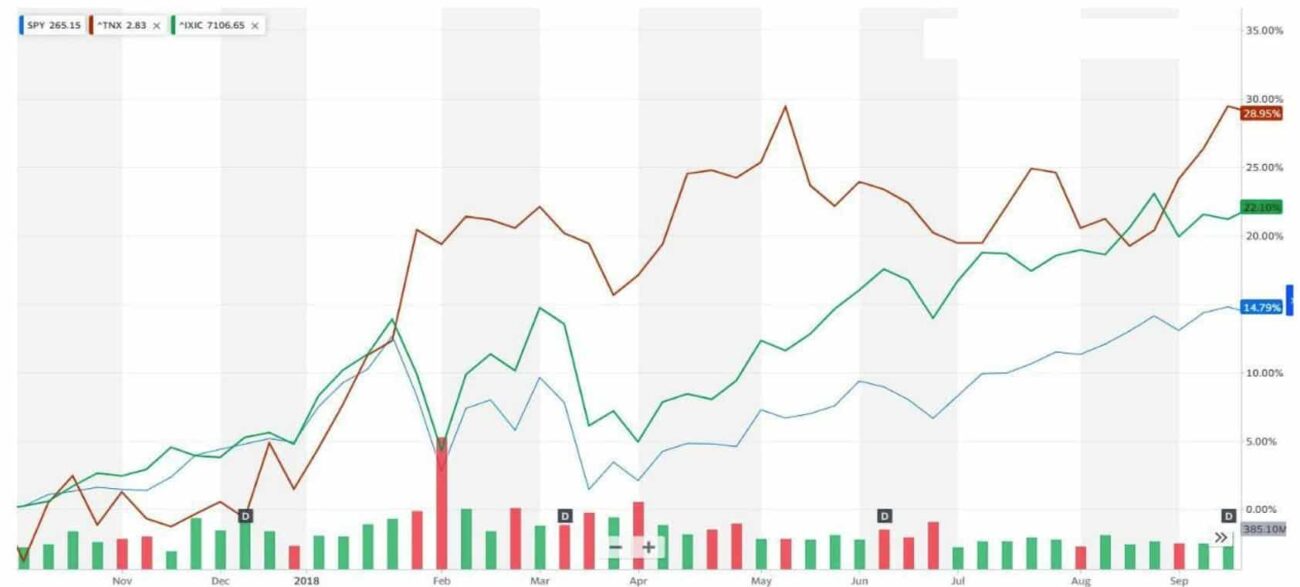

CNBC is full of pundits saying that the technology sector will not do well with rising interest rates. I believe they say that because it happened for a week. Very often, correlation is confused with causation. The last time we saw Treasury rates rise, was just a few years ago. From October 2017 to October 2018, the 10-year treasury yield rose from 2.2% to 3.1% (red line, today it is 1.75%). During that year, the Nasdaq rose 22.10% (green line) and the S&P 500 rose 14.79% (blue line); see chart from Yahoo Finance below.

The Standard & Poor’s 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. It is a market value weighted index with each stock’s weight in the index proportionate to its market value.

The Nasdaq Composite Index is a market-capitalization weighted index of the more than 3,000 common equities listed on the Nasdaq stock exchange. The types of securities in the index include American depositary receipts, common stocks, real estate investment trusts (REITs) and tracking stocks. The index includes all Nasdaq listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds (ETFs) or debentures.

During that time, the Fed raised rates four times, raising from 1.16% to 2.2% (current rate is 0.08%). Expectations are the Fed will raise three or four times over the next twelve months. Four raises would put the Fed Funds Rate just at or below where the rate started in the period above. Though three hikes are priced in and a fourth has a 40% expectation, I believe the Fed will have a hard time politically, raising a third time, much less a fourth.

Inflation, last year, was 6.8%, the highest since 1981, and is expected to hit 7% in Q1 of 2022. With the additional expectation of the supply chain easing, the Fed projects that inflation will drop to 2.6% by the end of the year. If that turns out to be nearly correct, there would be no reason for the Fed to hike a third or fourth time near year-end.

Supply Chain

Supply Chain

The supply chain has been choked due to a number of reasons. Foremost is the lack of truckers to carry the goods from port, exacerbated by the laws in California that prohibit non-union drivers. Union drivers only comprise about 40% of all truckers and since 40% of all U.S. imports arrive in two southern California ports, that creates a huge problem. Several larger companies like Walmart and Target, have leased ships and containers and are now shipping from Asia, through the Panama Canal and off-loading in Texas and Florida ports, but smaller companies do not have that option. This is a good reason we believe that this year, like the last ten, will not favor smaller companies. Add potentially higher interest rates which are more damaging to smaller companies, due to more limited options for borrowing, and we expect the Russel 2000 to once again, underperform.

Another advantage for large cap companies is their access to productivity tools. They can bankroll the more expensive tools like robotics, while other companies are more limited to software tools. No doubt, there are many software solutions, and they are helping all companies to become more profitable and provide better solutions and services. In our own business, we have seen how software has leveled the playing field for us and allows us to offer (what we consider) a more personal and effective offering than the biggest of companies. The software is a six-digit cost – we are fortunate that robotics is not a benefit in investment management and financial planning. Those can be 7 to 10-digit solutions, preventing most smaller-cap companies from employing them. Amazon is said to have over 600,000 robots helping their human warehouse force.

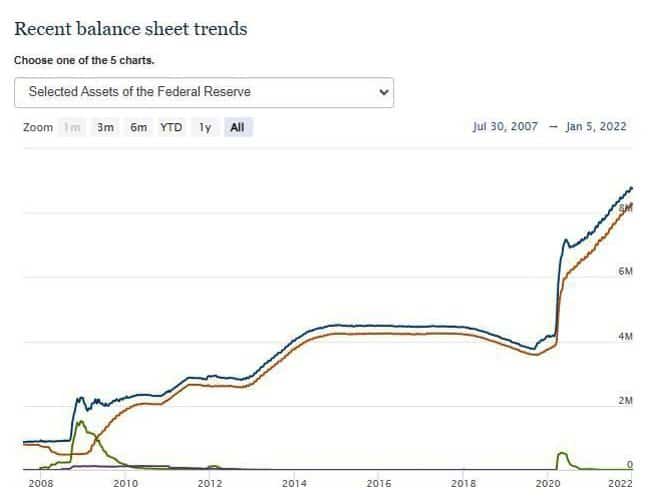

Fed Taper – Reducing the Balance Sheet

Fed Taper – Reducing the Balance Sheet

The Fed’s & Jerome Powell (Chairman) will face the difficulty of raising interest rates (above), but the more effective tool for fighting inflation will likely be the reduction in their balance sheet. “Taper” is simply printing less money each month which is used, primarily, to buy U.S. Treasuries. If the government is spending billions of dollars beyond their tax income, the debt will grow, and long-term interest rates may slightly rise. When the government starts spending trillions of dollars, the Fed is compelled to print trillions. $Trillions of new treasuries cannot be absorbed by the market. If the Fed withdraws/tapers its buying of treasuries, the federal government will need to wean themselves from the huge spending they’ve come accustomed to since COVID became a reason and then a convenient excuse. If they continue to pass trillion-dollar spending bills, we will adjust our portfolios, in an attempt to benefit from much higher interest rates. See the Fed balance sheet:

Addressing Inflation

Our portfolio currently has a hedge against inflation, serving us a dual purpose. We started adding oil & gas exploration companies to our portfolio when Joe Biden was inaugurated. It made sense to us since he had not made it a secret that he would restrict drilling, fracking, and pipelines. That combination would limit new supply and drive oil prices higher, making exploration companies more profitable. Our focus was on those companies with attractive land leases and that were able to manage thru the low oil prices of the previous years. We increased the position throughout the year and now have an energy weighting that is more than four times that of the S&P 500. Oil and other commodities also happen to be a good inflation hedge and our current weighting for, other than oil, commodities is three times that of the S&P. Finally, our weighting of commercial real estate is seven times that of the S&P (the three categories combined are slightly over 35% of our portfolio). None of these investments are simply inflation hedges. As for other commodities, we focused, more specifically on aluminum and copper. It is our thesis that both are heavily used in automobiles and even more so, in electric vehicles. Of course, copper is used extensively in homes and the number of homes in America is far below current and near-future demand.

Our commercial real estate provides a very good hedge against inflation while providing us attractive dividend income. The real estate is diversified by use, including data centers, warehouses, storage, and grocer-anchored shopping centers, to name a few. We believe our real estate holdings will continue to rise in value as COVID diminishes. Should inflation be more than transitory, it is our belief that the inflation will simply be adding more wind at the backs of all three sectors.

Defined Parameter

In a year that most economists are expecting high single digit or low double digit returns, Defined Parameter investments are a logical choice, and we are increasing those in our portfolios, along with oil, where we expect outsized gains. Defined Parameter allows us to balance downside protection with upside potential over the course of 12 months. We may choose from 9% to 15% downside protection, with 8% to 15% (typical range) upside participation. If the underlying index (S&P, Nasdaq, European, etc.) drops, we will lose nothing up to the downside protection. With 10% protection, an 8% drop would lose none of the investment, while a 12% drop would result in a 2% loss. By the same, if the 10% protection carried a 13% cap, we would enjoy the first 13% gain while a 17% gain in the index would still cap our gain at 13%. These are fully liquid, so we can invest in them in the middle of the 12-month period, and we can sell them during the 12 months (as we have in the past when the cap is close to being approached when several months remain).

This is the same concept that brought the popularity of insurance company, equity-indexed annuities. But don’t be fooled. Insurance companies have long lockups, and they simply cannot make attractive offerings with bond yields so low. However, they can make attractive printouts and promises. But like Nancy Reagan’s anti-drug saying, “Just say No”.

Regardless of how you are approaching the New Year, we wish you all the best in achieving your resolutions, goals, and aspirations. Most of all, we wish you a fantastic and fulfilling year because, as Van Morrison sang, “…time seems to go by so fast/In the twinkling of an eye/Let’s enjoy it while we can” and before its 2023!

From all of us, Happy New Year, The Beck Capital Management Team

January 2022 www.beckcapitalmanagement.com. 512.345.6789

Investment advisory services offered through Beck Capital Management, a registered investment adviser.

This material represents an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This newsletter contains forward-looking statements. Forward-looking statements are subject to certain risks and uncertainties and may not occur as presented. Actual results, performance, or achievements may differ materially from those expressed or implied.

Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor.

The Russell 2000 Index is an unmanaged index that measures the performance of the small-cap segment of the U.S. equity universe.

All investments involve risk, and the past performance of a security or financial product does not guarantee future results or returns. There is always the potential of losing money when you invest in securities or other financial products. The price of a given security may increase or decrease based on market conditions and customers may lose money, including their original investment.

Nothing contained herein is to be considered a solicitation, research material, an investment recommendation or advice of any kind. The information contained herein may contain information that is subject to change without notice. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. Product suitability must be independently determined for each individual investor. Investors should consider their investment objectives and risks carefully before investing. Beck Capital Management explicitly disclaims any fiduciary responsibility or any responsibility for product suitability or suitability determinations related to individual investors, as may relate to the information contained herein.