stocks and bonds

Yes, August was the worst month for the Dow in sixteen months. With anticipation of the Federal Reserve’s possible monetary tightening this month, and the “red line” in Syria, the October 1st start of some Obamacare provisions and the expected battle over the debt ceiling, many investors fled the markets. You can expect them back when those worries abate. That, to some extent, was witnessed yesterday when the market started the day very bullish on President Obama’s backtracking on Syria over the weekend (war less likely). It turned on Senator Boehner’s remarks that he would back the President on whatever the President thought prudent (war more likely). As the day wore on, investors began to believe that left up to President Obama, any decision is likely to be deferred another week as he travels abroad, and the longer it is deferred, the less likely it becomes.

Yes, August was the worst month for the Dow in sixteen months. With anticipation of the Federal Reserve’s possible monetary tightening this month, and the “red line” in Syria, the October 1st start of some Obamacare provisions and the expected battle over the debt ceiling, many investors fled the markets. You can expect them back when those worries abate. That, to some extent, was witnessed yesterday when the market started the day very bullish on President Obama’s backtracking on Syria over the weekend (war less likely). It turned on Senator Boehner’s remarks that he would back the President on whatever the President thought prudent (war more likely). As the day wore on, investors began to believe that left up to President Obama, any decision is likely to be deferred another week as he travels abroad, and the longer it is deferred, the less likely it becomes.

Since the debt ceiling has been battled many times before, it is already assumed to be less of an issue. The Fed’s quantitative tapering has been factored in, to a large extent, at the end of May and the middle of June after Ben Bernanke’s tapering speeches led many to believe that the September meeting will be the start. Personally, I do not expect that and have written the Fed, Barron’s, and Forbes regarding my own plan of tapering – a $4.25B/month reduction, taking the $85B/month printing to zero in 20 months.

Is there any dry powder?

I hear it every day … Someone asks: “Is there any dry powder to extend the rally?” In fact, I believe I’ve been hearing this asked since around late 2009, after just six or eight months of a rally. I wish it was a simple answer. On the one hand, the Fed has made cash, trash. And CDs are simply a safe way to go broke slowly (quoting my father). Bonds pay little interest and are likely to decrease in value while bond funds are destined for slaughter. Since 2007, investors have pulled $900 billion from stock funds while plowing a net of over 1.1 trillion new dollars into bond funds. If interest rates were to rise by just 1%, bond funds would lose at least 10% of their value and should rates rise by 2%, they may drop by 30% or more as investors head for the door and fund managers are all forced to sell their best bonds in a buyer’s market. So, if interest rates continue to rise we could see a steady flow of money from bonds to stocks and if they rise significantly (> 2%) we will see the money markets fill quickly and a subsequent supply of new equity dollars that could last many more years.

I hear it every day … Someone asks: “Is there any dry powder to extend the rally?” In fact, I believe I’ve been hearing this asked since around late 2009, after just six or eight months of a rally. I wish it was a simple answer. On the one hand, the Fed has made cash, trash. And CDs are simply a safe way to go broke slowly (quoting my father). Bonds pay little interest and are likely to decrease in value while bond funds are destined for slaughter. Since 2007, investors have pulled $900 billion from stock funds while plowing a net of over 1.1 trillion new dollars into bond funds. If interest rates were to rise by just 1%, bond funds would lose at least 10% of their value and should rates rise by 2%, they may drop by 30% or more as investors head for the door and fund managers are all forced to sell their best bonds in a buyer’s market. So, if interest rates continue to rise we could see a steady flow of money from bonds to stocks and if they rise significantly (> 2%) we will see the money markets fill quickly and a subsequent supply of new equity dollars that could last many more years.

The “many more years” of my view are predicated on the belief that though the U.S. has returned to a somewhat anemic growth, especially compared to what would be expected after a deep recession, it is still growth. The job market is especially anemic, but even 170,000 jobs per month are adding paychecks. And don’t forget this is a global market. Even China, with its “slowdown”, is still creating well over 1 million jobs each month. Add the rest of Asia, South America and parts of Africa and you have a lot of new paychecks looking for goods. Back at home, the American consumer has paid-down their debt whether the old-fashioned way or via bankruptcy so there is a tremendous amount of leverage which can be added over time. Finally, real estate has been climbing in value in most parts of the country, buoyed by low interest rates and of course, the stock market has added to the pocketbooks of slightly over half of the population. So in the short-term there is still a supply of dollars left in money market accounts and bank checking and savings. These, along with a slow rotation from low-yielding bonds could sustain the bull market in stocks for years.

But How Expensive Are stocks?

World indexes show the average price to projected earnings multiple at just 13.5 so stocks are not egregiously expensive, hence I would say it impossible to argue the world is significantly overweight equities and certainly not underweight bonds. A recent Gallup poll showed that just 52% of Americans own stocks compared to 65% in 2007 – that leaves a lot of investors still standing on the sideline – many wondering when and how to re-enter. This too was evidenced just last week when investors actually bought stocks on the news that 2nd quarter GDP was revised up to 2.5% from the 1.7% estimate. Hopefully, that marks the next era when good news is good for the market. For months, the market reacted positively to bad economic news under the belief that the Fed would continue printing, while good news was poorly received. I like the idea that good news will be good and bad news will be bad (again).

What about Gold, China and Emerging Markets?

I’ll preface that those of you who have known me a while, know that I was a gold, China, and emerging markets bull from 2003 thru 2011. It took the Fed’s QE2 to make me exit China and other emerging markets while QE3 was the death nail to gold. I expect tapering to help all three.

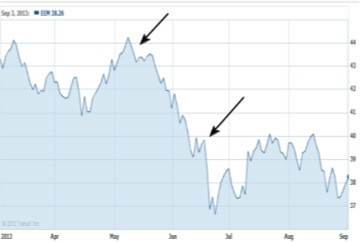

Since the May 22nd Bernanke speech, traders across the globe have been unwinding the so-called “carry trade”. This strategy has been a favorite of hedge funds and institutional investors since the depths of the financial crisis, when the Fed’s low interest rate policies encouraged yield-hungry investors to seek better opportunities than the zero percent US environment.

Here’s how the carry trade works: a trader buys a high-yielding currency, like the Brazilian real, and concurrently, sells a low yielding one, like the US dollar. The trader collects the interest-rate differential between the two. Sounds great until one or both parts of the trade move against the trader. In this case, that occurred when Ben Bernanke started talking about tapering bond purchases and in response, U.S. interest rates began to rise.

Since then, investors have been unwinding the trade and fleeing emerging markets, returning to the US, where the yield on the 10-year spiked from 1.6% in early May to 2.86% today. The shift in trading strategy is a short-term one, but one that can be disruptive, sending emerging markets lower. (see chart below with arrows on the two speeches).

Once the tapering schedule is known, emerging markets capital flight will complete. The threat of tapering has led to massive amounts of capital fleeing all the emerging markets, so much of that damage has already been realized. I believe the opportunity is at hand, however we will wait to hear the Fed on September 18th before considering a re-entry to China or other emerging markets. An announced plan will give us an opportunity to capitalize on a strengthening China without the risk of capital flight.

Once the tapering schedule is known, emerging markets capital flight will complete. The threat of tapering has led to massive amounts of capital fleeing all the emerging markets, so much of that damage has already been realized. I believe the opportunity is at hand, however we will wait to hear the Fed on September 18th before considering a re-entry to China or other emerging markets. An announced plan will give us an opportunity to capitalize on a strengthening China without the risk of capital flight.

So, When does the fed stop quantitative easing?

The mantra of “what will happen when the Fed stops the money-printing?” continues to drone on with every jobs report, monthly GDP, real estate reports or just about any other report that comes in above ZERO. How about the simple answer: Not in our lifetimes, or more realistically, at least not quickly. If Bernanke and the Fed stop printing and buying the newly issued Treasuries without Washington D.C. reducing spending dramatically, interest rates will jump (and don’t count the reduction due to the influx of tax payments received in April from taxpayers selling their gains in December to get ahead of the 2013 tax hikes – those taxes are now paid and have robbed the future, making deficits even higher in subsequent years). If interest rates just rise to the levels of 2006, it will add another $400 billion to our debt cost each year, doubling the 2006 and current costs, making the total over $800 billion/year. To put that $800 billion into perspective, prior to 2009, we only had a $400 billion deficit at the height of the Iraq and Afghanistan wars in 2004 and during the depression of 2008.

In 2007, the debt was almost exactly half what it is today, but interest rates were double – or go back to 1998 when the debt was just 1/3 what it is today, yet we paid the same in interest as we did last year – those rates would raise our annual interest cost to well over $1 Trillion. Bernanke will not allow rates to rise. He may resign and go teach at Princeton next January, but you can be sure that his successor (Larry Summers or Janet Yellen) will certainly continue the printing.

Flip this over and imagine what it would do to our exports if we quit the printing and allowed the dollar to strengthen while the U.K., Japan, and most other countries continued to print. A Ford might cost a billion yen but a Lexus could be a common high school graduation present here in the States. Our manufacturing would all but cease, laying off thousands of workers.

Bottom line:

Until you see our government on a real and sustainable path to eliminating deficit spending, with our GDP and jobs markets growing, and the rest of the world backing off their printing presses, you need not wonder when our Fed will turn off the printers. They won’t!

The only reasonable answer is to invest in a manner that will ultimately outpace the currency devaluation. Owning real estate, equities of growing companies which own hard assets and pay reasonable dividends, and rotating your portfolio as needed over time. A good example are banks and homebuilders. We owned them for years while interest rates favored them, but sold them all in early 2007 and did not buy them again until December of 2011, almost five years later shortly after the Fed began purchasing their mortgage-backed securities (the worst bank assets) and began purchasing Treasuries in an effort to help reduce mortgage rates. Recently, the multiple airline mergers changed my lifetime thesis of never owning airlines. They are now a large position and have done very well for us. Considering I always said that if God had meant man to fly, he would have made airlines profitable; that is keeping an open mind.

Here’s to always keeping an open mind and challenging ourselves,

Frank

Disclosure: Nothing contained herein is to be considered a solicitation, research material, an investment recommendation or advice of any kind. The information contained herein may contain information that is subject to change without notice. Any investments or strategies referenced herein do not take into account the investment objectives, financial situation or particular needs of any specific person. Product suitability must be independently determined for each individual investor. Frank Beck & Beck Capital Management explicitly disclaims any responsibility for product suitability or suitability determinations related to individual investors. The investment products discussed herein are considered complex investment products. Such products contain unique risks, terms, conditions and fees specific to each offering. Depending upon the particular product, risks include, but are not limited to, issuer credit risk, liquidity risk, market risk, the performance of an underlying derivative financial instrument, formula or strategy. Return of principal is not guaranteed above FDIC insurance limits and is subject to the creditworthiness of the issuer. You should not purchase an investment product or make an investment recommendation to a customer until you have read the specific offering documentation and understand the specific investment terms and risks of such investment.

This material represents an assessment of the market and economic environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Forward-looking statements are subject to certain risks and uncertainties. Actual results, performance, or achievements may differ materially from those expressed or implied. Information is based on data gathered from what we believe are reliable sources. It is not guaranteed as to accuracy, does not purport to be complete and is not intended to be used as a primary basis for investment decisions. It should also not be construed as advice meeting the particular investment needs of any investor. Past performance does not guarantee future results.